Beyond the Power Law

Where patience, resilience, and compounding value create the next generation of markets...

...and where resilience is the new alpha

The Problem

Classic venture capital was built for software - rapid growth, high valuations, quick exits.

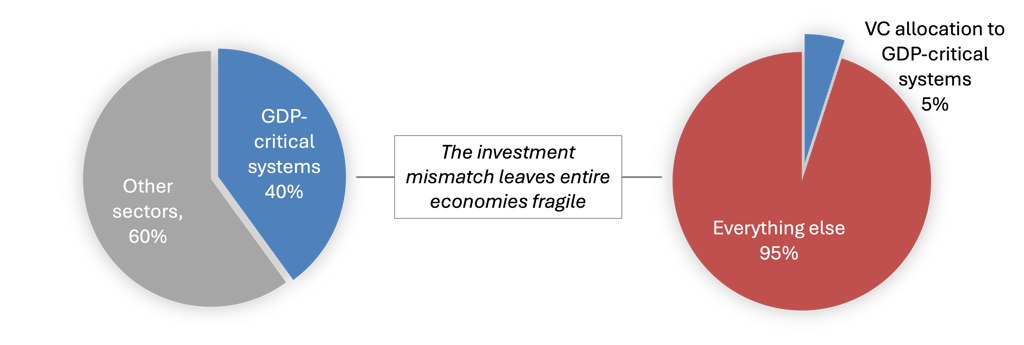

But ag, food, energy, water, health, and materials - sectors that over 40% of global GDP rely upon - move slower and face longer exit clocks.

These sectors attract less than 5% of VC flows globally.

The mismatch is a drag on GDP.

40%

<5 %

VC allocation

GDP

Resilience as Alpha

For 200,000 years, human prosperity was aligned with the rhythms of natural systems. The industrial era broke that bond, creating extractive models that delivered progress but left GDP-critical sectors fragile and exposed.

Restoring resilience is not ethics or philanthropy. It’s basic economics. The systems we rely on – food, energy, water, health, and infrastructure – are constrained by ecological volatility, regulatory shifts, social pressure, and geopolitics. These are not passing headwinds. They are structural forces that will shape capital flows, industrial strategy, and consumer behavior for decades.

Resilience is no longer a defensive posture.

It is the alpha driver of the next economy.

The Fix:

A New Risk Architecture

Most VC is reactive and Power Law dependent – a model that fails in regulated, resilience-driven sectors where exits are slower and capital arrives too late.

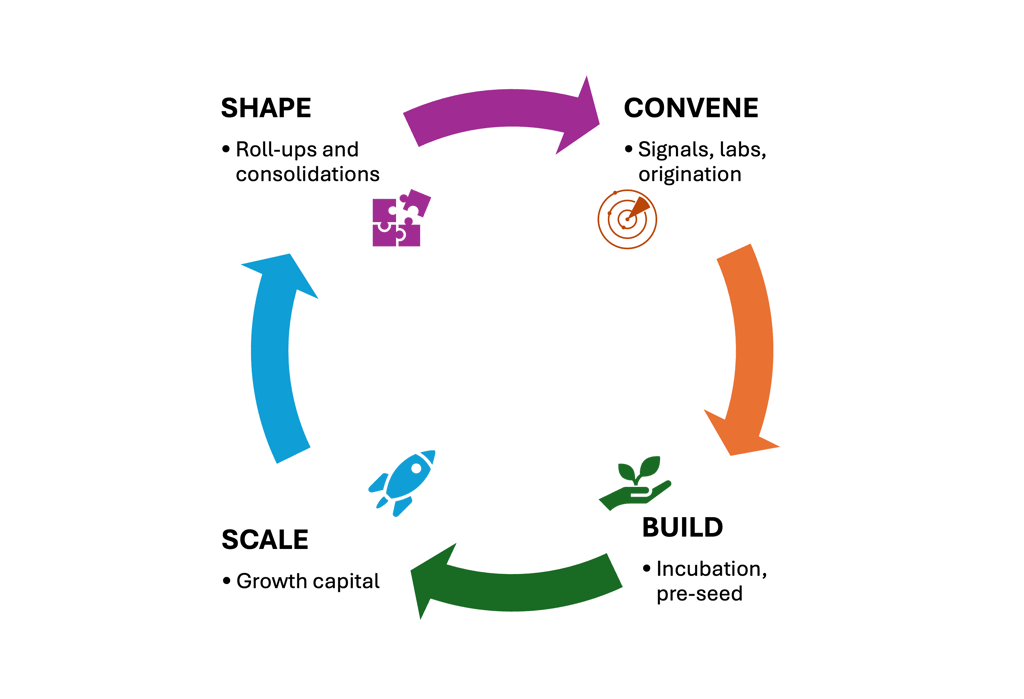

The solution is a different type of risk architecture altogether - a flywheel that continually generates, scales, and compounds opportunity. One that puts resilience and returns in the same sentence.

Originate ventures at collision points between existing verticals, incubate what incumbents can’t, scale the best, and consolidate winners into durable platforms. A closed loop that turns fragility into compounding value.

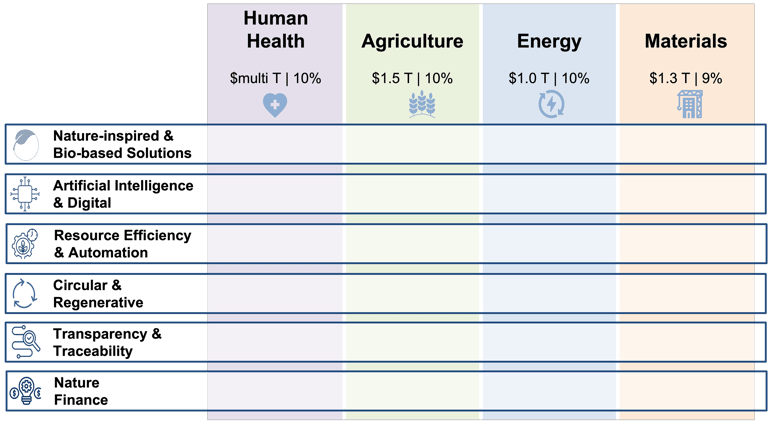

Where to Hunt

Collision Points = New Markets

The future will be won by creating new industries and categories. Mature spaces cannot do this because there, incumbents are fortified, and their innovation capabilities are contracting due to the emphasis on defending their territory.

The next wave of enterprise value will be built at the boundaries - collision points where foundational systems meet. For example, Ag × Computation; Energy × Biology; Health × Materials. At these interfaces, new entrants have room to operate and compound because the boundaries are still forming.

For investors, these collision points are system-level leverage points where new categories can be written before moats harden and regulatory regimes lock in. This creates the rarest condition in modern venture: spaces that are both critical yet underfunded.

Why Now

The mismatch between VC and GDP-critical systems is now an economic liability.

Valuations are being reset, talent supply is strong: a once-in-decades vintage tailwind.

Science is colliding with real economies faster than incumbents can absorb.

Capital innovation (DFIs, blended finance) is stacking with venture equity.

Call to Action

Strategy Validation

What’s the single biggest risk you see that could keep this model from working?

Which collision points (sector intersections) feel most investable in the next 24 months?

Where does the “flywheel” architecture (Convene → Build → Scale → Shape) feel robust or fragile?

Investor Lens

Which part of this model most challenges your current allocation framework?

What data or proof point would build conviction fastest?

What existing vehicle does this most resemble? Where is it most differentiated?

Next Steps

Which 1-2 LPs or strategics should this be in front of?

If you were me, where would you focus pipeline proof first?

Should this be structured as a traditional fund, a permanent holding company, or a hybrid?

hello@BeyondThePowerLaw.com

© 2025. All rights reserved.